How to Withdraw EPF online?

The Government of India will pay the employer and employee contribution to EPF account of employees for another three months from June to August 2020. The benefit is for establishments with up to 100 employees and where 90% of those employees draw a salary of less than Rs 15,000 per month. The contribution to EPF is reduced to 10% from 12% for non-government organisations.

EPF (Employees’ Provident Fund), also referred to as PF (Provident Fund), is a mandatory savings cum retirement scheme for employees of an eligible organisation. This fund is intended to be a corpus on which the employees can fall back on in their retired life. As per the EPF norm, the employees must contribute 12% of their basic pay every month. A matching amount is contributed by the employer as well. The amount deposited in EPF accounts earns interest on an annual basis. Employees can withdraw the entire sum accumulated in their EPF once they retire. However, premature withdrawals can be made on meeting certain conditions.

Employees’ Provident Fund Organisation has allocated UAN, i.e. the Universal Account Number compulsory for all the employees covered under the PF Act. The UAN would be linked to the employee’s EPF account. The UAN remains portable throughout the lifetime of an employee, and there is no need to apply for EPF transfer at the time of changing jobs.

EPF WITHDRAWAL

1. When can EPF be withdrawn

One may choose to withdraw EPF entirely or partially. EPF can be completely withdrawn under any of the following circumstances:

a. When an individual retires

b. When an individual remains unemployed for more than two months. To make a withdrawal on this circumstance, the individuals must get an attestation of the same from a gazetted office.

The complete withdrawal of EPF while switching employers without remaining unemployed for two months or more (i.e. during the interim period between changing jobs), is against the PF rules and regulations and therefore is not allowed. Partial withdrawal of EPF can be made under certain circumstances and subject to certain prescribed conditions which have been discussed in brief below:

Partial withdrawal of EPF can be done under certain circumstances and subject to certain prescribed conditions which have been discussed in brief below:

Sl. No. | Particulars of reasons for withdrawal | Limit for withdrawal | No. of years of service required | Other conditions |

1 | Medical purposes | Six times the monthly basic salary or the total employee’s share plus interest, whichever is lower | No criteria | Medical treatment of self, spouse, children, or parents |

2 | Marriage | Up to 50% of employee’s share of contribution to EPF | 7 years | For the marriage of self, son/daughter, and brother/sister |

3 | Education | Up to 50% of employee’s share of contribution to EPF | 7 years | Either for account holder’s education or child’s education (post matriculation) |

4 | Purchase of land or purchase/construction of a house | For land – Up to 24 times of monthly basic salary plus dearness allowance For house – Up to 36 times of monthly basic salary plus dearness allowance, Above limits are restricted to the total cost | 5 years | i. The asset, i.e. land or the house should be in the name of the employee or jointly with the spouse. |

5 | Home loan repayment | Least of below:

| 10 years | i. The property should be registered in the name of the employee or spouse or jointly with the spouse. ii. Withdrawal permitted subject to furnishing of requisite documents as stated by the EPFO relating to the housing loan availed. iii. The accumulation in the member’s PF account (or together with the spouse), including the interest, has to be more than Rs 20,000. |

6 | House renovation | Least of the below: Up to 12 times the monthly wages and dearness allowance, or Employees contribution with interest, or Total cost | 5 years | i. The property should be registered in the name of the employee or spouse or jointly held with the spouse. |

7 | Partial withdrawal before retirement | Up to 90% of accumulated balance with interest | Once the employee reaches 54 years and withdrawal should be within one year of retirement/superannuation |

Broadly, the withdrawal of EPF can be made either by:

- Submission of a physical application for withdrawal

- Submission of an online application

To apply for the withdrawal of EPF online through the EPF portal, make sure that the following conditions are met:

- The UAN (Universal Account Number) is activated, and the mobile number used for activating the UAN is in working condition.

- The UAN is linked with your KYC, i.e. Aadhaar, PAN and the bank details along with the IFSC code.

If the above conditions are met, then the requirement of attestation of the previous employer to carry out the process of withdrawal can be done away with.

Steps to apply for EPF withdrawal online:

Step 1: Go to the UAN portal by clicking here.

Step 2: Log in with your UAN and password and enter the captcha.

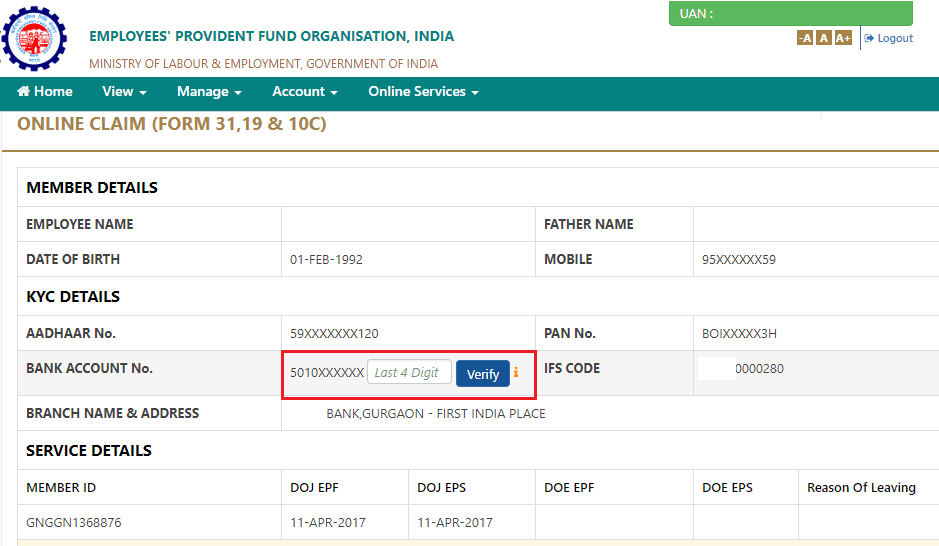

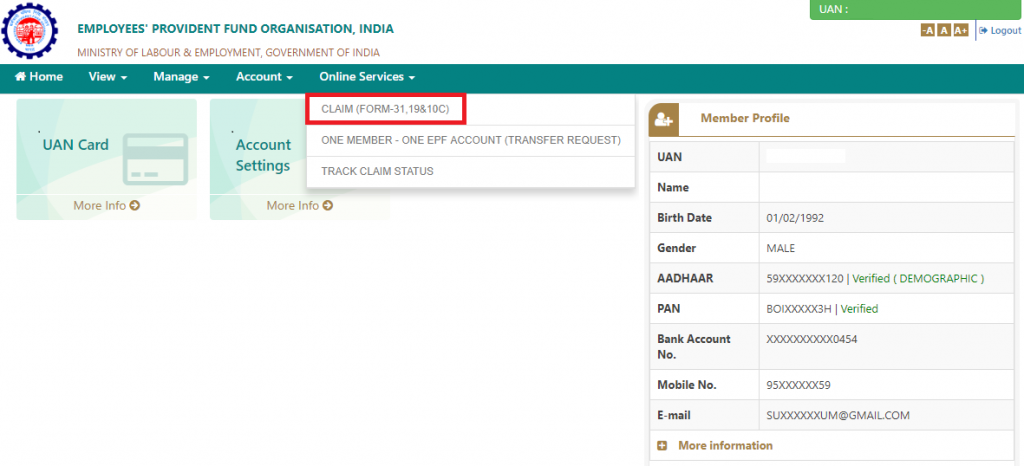

Step 3: Then, click on the tab ‘Manage’ and select KYC to check whether your KYC details such as Aadhaar, PAN and the bank details are correct and verified or not.

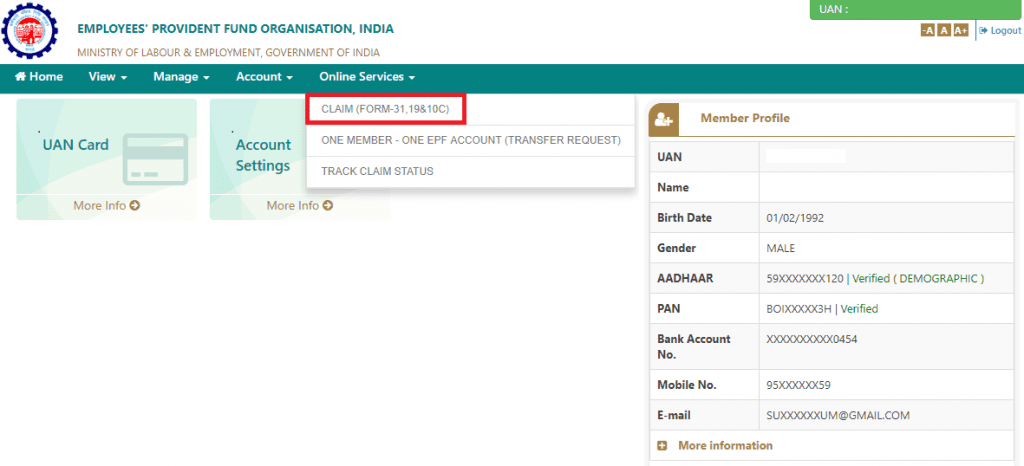

Step 4: After the KYC details are verified, go to the tab ‘Online Services’ and select the option ‘Claim (Form-31, 19 & 10C)’ from the drop-down menu.

Step 7: Now, click on ‘Proceed for Online claim’.

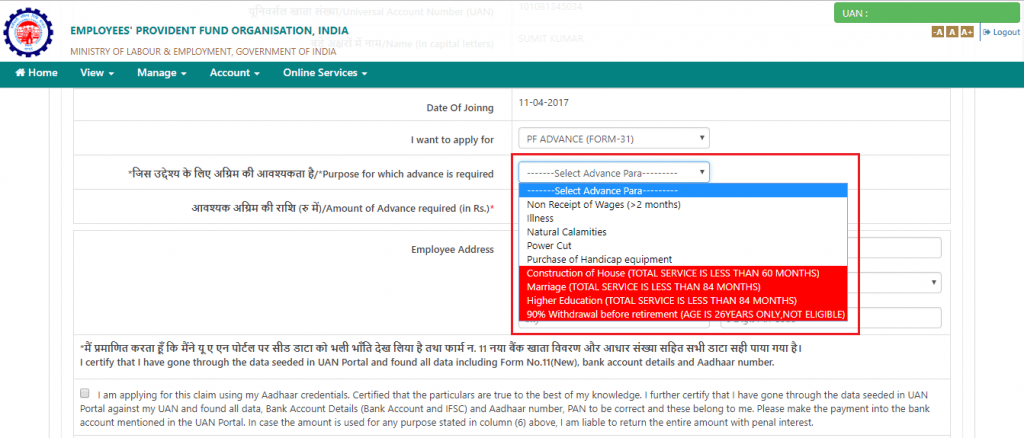

Step 8: In the claim form, select the claim you require, i.e. full EPF settlement, EPF part withdrawal (loan/advance) or pension withdrawal, under the tab ‘I Want To Apply For’. If the member is not eligible for any of the services like PF withdrawal or pension withdrawal, due to the service criteria, then that option will not be shown in the drop-down menu.

Step 9: Then, select ‘PF Advance (Form 31)’ to withdraw your fund. Further, provide the purpose of such advance, the amount required and the employee’s address.

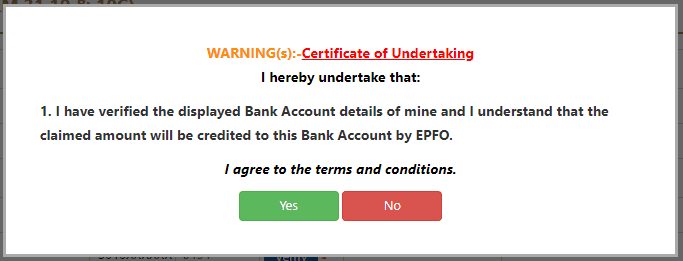

Step 10: Click on the certificate and submit your application. You may be asked to submit scanned documents for the purpose you have filled the form. The employer will have to approve the withdrawal request and then only you will receive money in your bank account. It usually takes 15-20 days to get the money credited to the bank account.

3. How to Apply for Home Loan Based on EPF Accumulation?

You can follow the procedure given below to apply for a home loan based on your EPF account balance:

Step 1: Apply for a home loan through the housing society to the EPF Commissioner in the format specified in Annexure 1.

Step 2: The Commissioner will issue a certificate which states the monthly contribution to your EPF account over the last three months. Alternatively, you can take a printed copy of your EPF passbook to show the last three months contribution.

Step 3: You can opt for a lump sum payout or instalments.

Step 4: EPFO makes the payment to the housing society directly.

Still have doubts in your mind regarding the EPF withdrawal, comment below your doubts.

{kind=link}