Residents with Foreign Income Tax Returns Filing

Indian residents with foreign income or income from stock options in foreign entities must pay taxes on such income in India. Get CA assistance in filing your income returns. Taxability of Income in India depends on your residential status in India, the source of Income and the place of receipt of Income. Your residential status is determined based on your physical presence in India in the current financial year (FY) and the preceding 10 FYs. If you qualify as a resident and ordinarily resident in India, your global income will be taxable in India as per the India income-tax law. You must report all your assets outside India (such as bank accounts, immovable property and financial interests) in your income tax return in detail. If you qualify either as a non-resident or resident but not ordinarily resident in India, then as per Income-tax, you'll be taxable on following incomes:

a. Income received in India or deemed to be received in India.

b. Income accruing or arising in India or deemed to accrue or arise in India.

Tax Filing Simplified for Indian residents with foreign income. Get your tax filed by TAXAJ Experts

It usually takes 1 to 2 working days.

- CA Assisted Filing of your Income Tax returns

- CA Assisted Filing of your Form 67 on Income Tax portal (if required)

- Email/Skype/Calling Support

- Includes foreign & domestic income and resulting tax liabilities

- Handling complexities of taxation in multiple countries, availing double taxation avoidance agreements (DTAA)

- Declaration of foreign assets for Indian residents (Schedules FA, FSI and TR in the Income Tax Return)

- Indian citizens working on-site, at client locations outside India

- Indian citizens who own a bank account or any other asset abroad

- Foreign nationals who work in India, who earn salary in India or have Indian assets *Indian Residents earning income from foreign entities

- Purchase of Plan

- Upload documents

- Review computation sheet

- Return filed & acknowledgement generated

- Form 16 from your company

- Form 26AS Tax Credit Statement

- Details of any Income earned in India

- Details of Income earned Outside India

- Bank statement if interest received is above Rs. 10,000/-

Income Tax For Residents having Foreign Income or Assets outside India.

Residential Status for Income Tax – Individuals & Residents

The Income Tax Department needs to determine the residential status of a tax-paying individual or company. This status is one of the factors based on which a person’s taxability is decided. It becomes particularly relevant during the tax filing season. Let us explore the residential status and taxability in detail.

Meaning and importance of residential status

The taxability of an individual in India depends upon his residential status in India for any particular financial year. The term residential status has been coined under the income tax laws of India and must not be confused with an individual’s citizenship in India. An individual may be a citizen of India but maybe a non-resident for a particular year. Similarly, a foreign citizen may be a resident of India for income tax purposes for a specific year. Also, to note that the residential status of different persons viz an individual, a firm, a company etc., is determined differently. In this article, we have discussed how the residential status of an individual taxpayer can be determined for any particular financial year.

How to determine residential status?

👉 A resident

👉 A resident not ordinarily resident (RNOR)

👉 A non-resident (NR)

Resident

As a taxpayer you would qualify as a resident Indian if you can satisfy either of the following conditions:

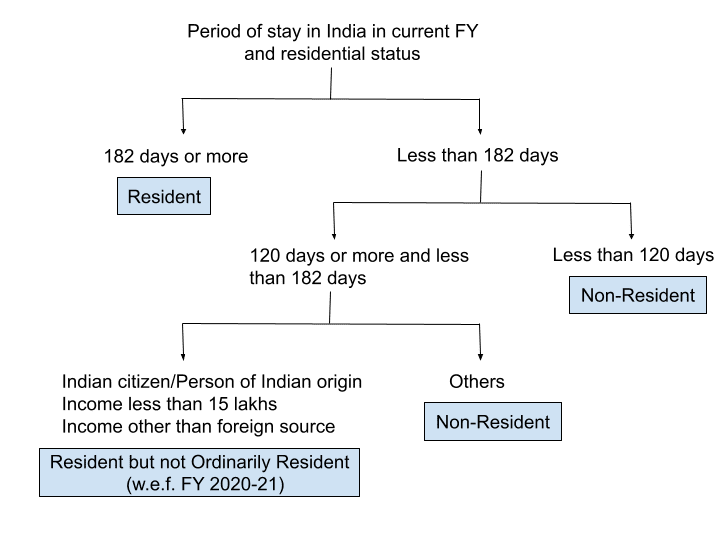

1. If you have stayed here in India for 182 days or more in a year.

2. If your stay here in India for last 4 preceding years exceeds 365 days or more. Addition to this 60 days or more in the relevant financial year.

Suppose an individual who is a citizen of India or person of Indian origin leaves India for employment during an FY. In that case, he will qualify as a resident of India only if he stays in India for 182 days or more. Such individuals are allowed a more extended time of 60 days and less than 182 days to stay in India. However, from 2020-21, the period is reduced to 120 days or more for such an individual whose total income (other than foreign sources) exceeds Rs 15 lakh.

In a new amendment from FY 2020-21, an individual who is Indian citizen & not liable to taxation in any foreign country will be deemed a resident in India. This condition applies only if the total income (other than foreign sources) exceeds Rs 15 lakh here in India & nil tax liability in other countries or territories because of his domicile or residence.

This vital amendment can be further simplified as below-

Resident not Ordinary Resident

If, as an individual, you qualify as a resident, the next step is to determine if you're a Resident ordinarily resident (ROR) or an RNOR. You'll be a ROR provided that you meet the following conditions:

1. You've been an Indian resident in at least 2 out of 10 last years immediate years.

2. You've stayed here for at least 730 days in the last 7 immediate years.

If you fail to satisfy even one of the two conditions provided above, you're an RNOR.

From FY 2020-21, an Indian Citizen or a person of Indian origin goes abroad for employment during the year will be treated as resident and ordinarily resident if he stays here for more than 182 days. However, this condition is applicable only if his total income here exceeds Rs 15 lakh (other than your foreign sources). Also, an Indian citizen who is deemed a resident here (w.e.f FY 2020-21) will be a resident and ordinarily resident in India.

NOTE: Income from foreign sources means income that accrues or arises outside India (except income derived from a business controlled in India or a profession set up in India).

If You qualify as a resident, the next step is to determine if you're a Resident ordinarily resident (ROR) or an RNOR. You're a ROR if you can fulfill following conditions:

1. Have been a resident of India in at least 2 out of last 10 immediate years.

2. Has stayed here for at least 730 days in 7 immediately preceding years

If you fail to satisfy even one of the two conditions provided above, you're an RNOR.

From FY 2020-21, an Indian Citizen or a person of Indian origin goes abroad for employment during the year will be treated as resident and ordinarily resident if he stays here for more than 182 days. However, this condition is applicable only if his total income here exceeds Rs 15 lakh (other than your foreign sources). Also, an Indian citizen who is deemed a resident here (w.e.f FY 2020-21) will be a resident and ordinarily resident in India.

NOTE: Income from foreign sources means income that accrues or arises outside India (except income derived from a business controlled in India or a profession set up in India).

Non Resident

An individual satisfying neither of the conditions stated in (a) or (b) above would be an NR for the year.

Taxability

Resident: A resident will be charged to tax in India on his global income, i.e. income earned in India and income earned outside India.

NR and RNOR: Their tax liability in India is restricted to the income they earn in India. They need not pay any tax in India on their foreign income. Also, note that in a case of double taxation of income where the same income is getting taxed in India and abroad, one may resort to the Double Taxation Avoidance Agreement (DTAA) to eliminate the possibility of paying taxes twice.

Tax on Foreign Income of Resident Indian

If you have a foreign asset, holding, stocks or any investment there that yields income, such an income is subject to taxation here as per applicable income tax rates. Please find the process in detail about including your foreign income in your income tax returns plan and to pay the applicable tax –

👉 Firstly, convert your foreign earnings into rupees. State Bank of India’s Telegraphic Transfer Buying Rate (TTBR) will be helpfull in doing so. The rate applicable on the last day of the month immediately preceding the month in which you earn the income. For example, if you earned the income in August 2021, use the TTBR of July 2021 for conversion of foreign revenue into Indian Rupees.

👉 Secondly, once the amount is converted, list it under foreign income. So, if you have earned a property income held in a foreign country, list the income under the head ‘Income from house property. If the income is a payment for your services rendered abroad, include it under ‘Income from salary. Always select relevant income head based on the nature of income and list the foreign income under that particular head.

👉 After clubbing the foreign income, it would be a part of your income earned in India. Now you will have to add up income from all the heads of income and calculate the gross taxable income.

👉 You can then deduct the allowed deductions and exemptions under different sections of the Income Tax Act applicable to derive the net taxable income. Calculate your tax liability on the net taxable income using the income tax slabs and pay the due tax.

TDS on Foreign Income

To avail of the benefit under DTAA, you would have to obtain a Tax Residency Certificate (TRC). This certificate helps identify your residential status for taxation purposes so that the right DTAA rule could be applied to your tax relaxation.

You can claim DTAA credit under following methods.

1. Exemption method- If the income is taxed in one country, it is exempted from tax in another country.

2. Tax credit method- If the Income is taxed in both countries then taxpayer can claim tax relief in his country of residence.

Declaring your income and liabilities in Income tax return is vital irrespective of place where you've earned them.

How to Claim Tax Credit on Foreign Income of a Resident?

Have you earned some foreign income while working abroad this financial year?

While working abroad, have they deducted some tax on your foreign income? If you are a Indian resident, then as per income tax, your income earned anywhere in the world is taxable here in India. But to know that how this income be included in your tax return? Explained here:

👉 Convert all your income generated abroad into Indian currency – convert by using SBI telegraphic transfer buying rate (TTBR) of previous months last date in which income is due. For example, for converting salary income of October 2021, use the TTBR of the relevant currency for September 2021 and convert your income to Rupees.

👉 Now, include these income as per their head e.g. Put salary income under the head ‘salaries.

👉 This income will be treated as any other income earned by you locally. Minimum Rs 2,50,000 exemption is allowed on your total income, remaining income will be taxable as per your tax slab.

👉 If TDS has already been deducted from your income, you are allowed to take credit for such taxes. For this purpose, reference must be made to the relevant Double Tax Avoidance Agreement (DTAA) of the country where you earned such income. India has entered into DTAAs with various countries to makes sure that you as a taxpayer is not taxed twice for single income earned abroad. Most of the times income is taxed at source where it is originated and as a resident of a particular country you're usually liable to pay tax in your country of residence. Here DTAA ensures that you're not adversely impacted. You're allowed to take credit of TDS.

👉 In order to Take benefit of DTAA you need to obtain Tax Residency Certificate (TRC) that helps identify and certify your tax residency status to make sure the correct DTAA has been applied. This is in line with the tax laws in India.

👉 While taking TDS credit, make sure you are referring to the correct DTAA. Under DTAA, there are two methods to claim tax relief – exemption method and tax credit method. By the exemption method, your income is taxed in one country and exempted in another. In the tax credit method, where the income is taxed in both countries, tax relief can be claimed in the country of residence.

👉 If no DTAA exists between the 2 countries, you may still be able to get a tax credit on foreign taxes paid. You may need an expert to assist you.

👉 In the latest income tax return forms, several disclosures have been added for income on which DTAA benefit has been claimed.

If you have earned foreign income on which TDS or any form of tax has been deducted, you may need help from an expert to obtain a TRC and make sure the correct DTAA is applied, so you can take credit for the foreign tax deducted.

- How do CA-Assisted Plans work?

Handling complex cases where foreign income is involved requires expert assistance. TAXAJ assigns a chartered accountant to you after payment. The CA contacts you and prepares your return. Finally, the CA e-files the income tax return after your review.

- Do you offer phone support in this plan?

Most of the support and assistance is offered over email. You can always schedule a phone call / Skype call with the CA at a time that’s convenient to you as per your time zone.

- How do I determine my residential status?

Your residential status for Income Tax purposes is based on the number of days you spend within India. If you are a foreign national living within India, you may be considered a ‘Resident Indian’ for tax purposes, and similarly if you are an Indian living abroad, you might be considered a Non-Resident Indian (NRI).

Typically, if you are in India for 182 days or more during that financial year, you will be considered a resident. There are a few more conditions associated with this.

- Who are the CAs who’ll be filing my return?

TAXAJ taps into its CA network and puts you in touch with a qualified CA. These CAs bring a combined experience of 40 years in foreign taxation.

- I hold stock of a foreign company as RSU/ESOPs. Which plan should I opt for?

This plan is the right plan for you. In this plan, a CA will prepare and submit your tax return to the IT Department. He will also fill out foreign income-specific schedules and check relevant compliance with regard to Double Taxation Avoidance Agreement.

- What is the cancellation / refund policy?

Refund is applicable only if no CA has been assigned on the case, for detailed policy please visit our terms of use

- How will TAXAJ file Form 67?

For filing Form 67, you will have to share your Income Tax login credentials to the CA assigned to your case.