Old Tax Regime v/s New Tax Regime

Individuals and HUF taxpayers are eligible to choose a new tax regime from FY 2020-21.

From FY 2020-21, you can choose to pay income tax under an optional new tax regime. The new tax regime is available for individuals and HUFs with lower tax rates and zero deductions/exemptions. We will discuss the features of the new tax regime and how you can benefit from it.

All you need to know to save your Income Tax for Comparing both Tax Regimes!

What is the new tax regime for FY 2020-21?

What is the new tax regime for FY 2020-21?

The Budget 2020 introduces a new regime under section 115BAC giving an option to individuals and HUF taxpayers to pay income tax at lower rates. The new system is applicable for income earned from 1 April 2020 (FY 2020-21), which relates to AY 2021-22.

What are the tax rates under the new regime?

What are the tax rates under the new regime?

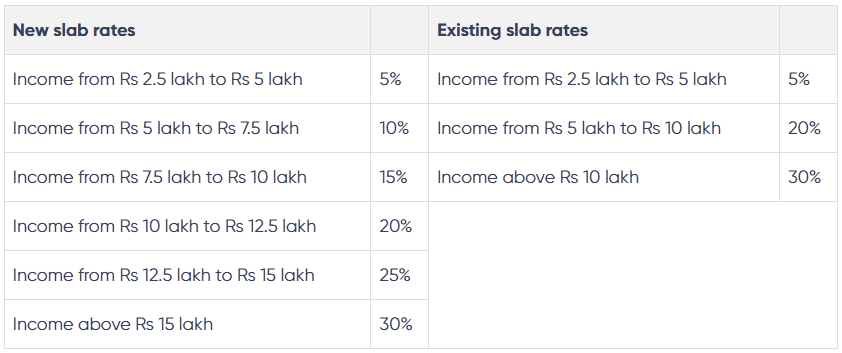

The tax rates under the new tax regime and the existing tax regime are:

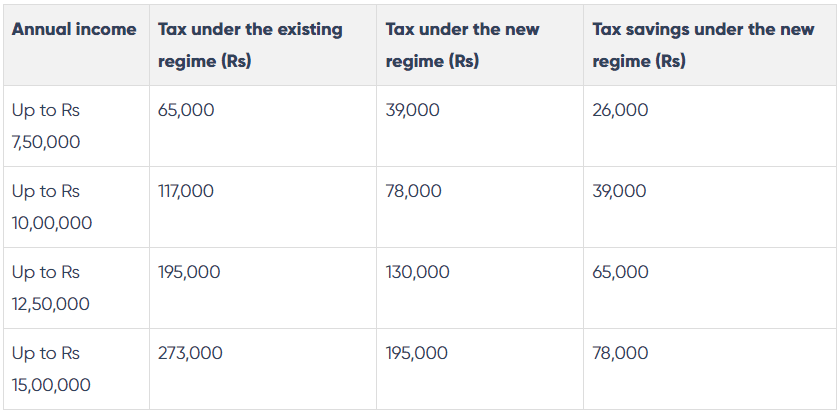

The new tax regime does not allow 70 deductions and exemptions (discussed in para 4). The tax payable under both the latest and the existing regimes without claiming deductions and exemptions is as below:

The new tax regime saves taxes for taxpayers who don’t claim any deductions or exemptions.

Exemptions and deductions not claimable under the new tax regime

Exemptions and deductions not claimable under the new tax regime

The following are the deductions and exemptions you cannot claim under the new tax system:

- The standard deduction, professional tax and entertainment allowance on salaries

- Leave Travel Allowance (LTA)

- House Rent Allowance (HRA)

- Minor child income allowance

- Helper allowance

- Children education allowance

- Other special allowances [Section 10(14)]

- Interest on housing loan on the self-occupied property or vacant property (Section 24)

- Chapter VI-A deduction (80C,80D, 80E and so on) (Except Section 80CCD(2) and 80JJAA)

- Without exemption or deduction for any other perquisites or allowances

- Deduction from family pension income

What are the exemptions and deductions available under the new regime?

What are the exemptions and deductions available under the new regime?

You can claim tax exemption for:

- Transport allowances in case of a specially-abled person.

- Conveyance allowance received to meet the conveyance expenditure incurred as part of the employment.

- Any compensation received to meet the cost of travel on tour or transfer.

- Daily allowance received to meet the ordinary regular charges or expenditure you incur on account of absence from his regular place of duty.

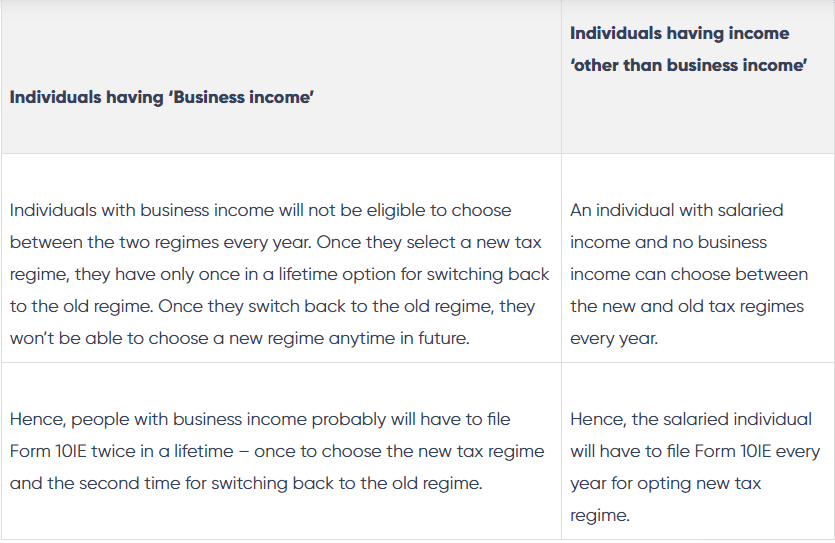

Can I choose between the new tax regime and the existing regime?

Can I choose between the new tax regime and the existing regime?

A salaried taxpayer can choose the new tax regime at the beginning of FY 2020-21 and intimate their employer. The employee cannot change their choice anytime during the financial year. However, the change can be done at the time of filing the income tax return in July 2021.

The due date for tax filing for the FY 2020-21 (AY 2021-22) is 30th Sep 2021 (extended from 31st July 2021).

In case an employee does not choose the new tax regime at the beginning of the financial year, the employer will deduct tax (TDS) under the existing tax regime. Hence, a salaried taxpayer can opt-in and opt-out every year. That means you can choose the new tax regime in one year and choose the regular tax regime in another year.

A non-salaried taxpayer has to choose the new regime at the time of filing the tax return. They need not declare or intimate their choice to anyone at any time during the year. However, a non-salaried taxpayer cannot opt-in and opt-out of the new tax regime every year. Once a non-salaried opts out of the new tax regime, they cannot opt-in again for the new tax regime in the future.

How do I choose the new regime and plan my tax?

How do I choose the new regime and plan my tax?

From a tax planning perspective, it is essential to choose the tax regime at the beginning of the financial year. A taxpayer must make a comparison of the income tax under the new tax regime with the existing regime. Once the taxpayer chooses the tax regime at the beginning of the year, the investments and TDS or advance tax payable calculations are made accordingly. Also the taxpayer has to furnish Form 10IE to the income tax department before filing the return if the taxpayer intends to opt for the new tax regime.

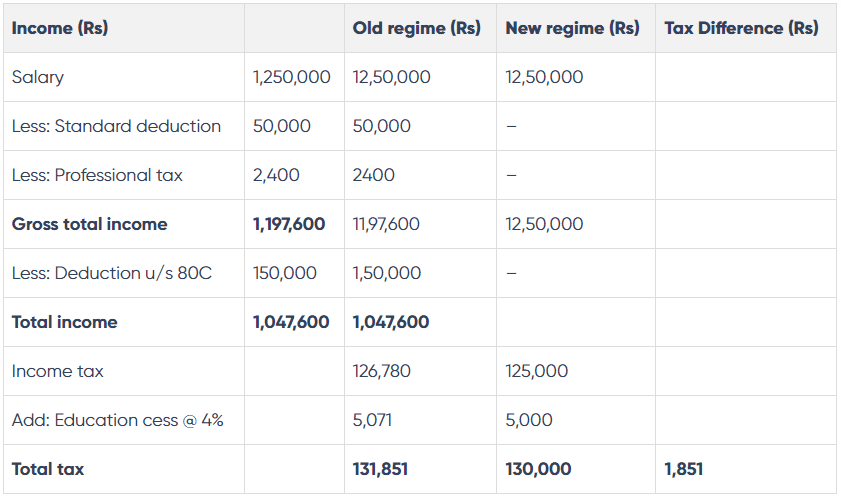

Example 1: Where New regime is better in respect of tax outflow

Example 1: Where New regime is better in respect of tax outflow

In the above example, for an income of INR 12,50,000, the new tax regime is marginally beneficial. However, if you claim further deductions for health insurance, investment in NPS, education loan and so on, the existing regime will be helpful in respect of tax savings.

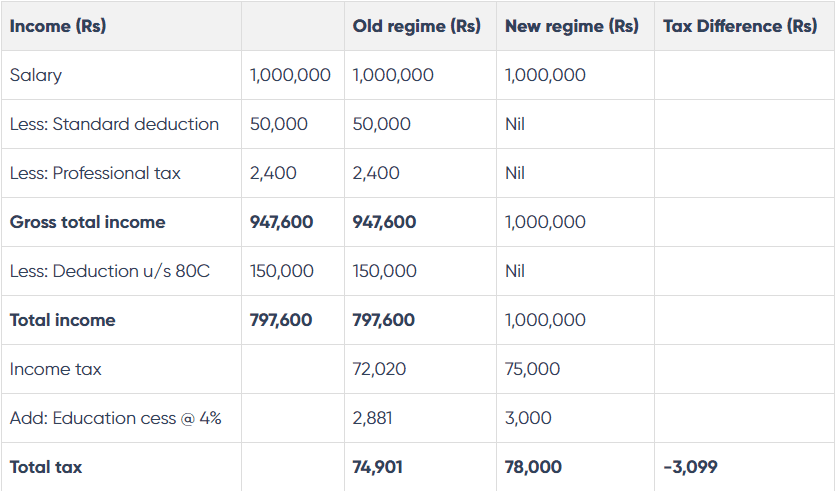

Example 2: Where Old regime is better in respect of tax outflow

Example 2: Where Old regime is better in respect of tax outflow

In Example 2, for an income of INR 10 lakh, the existing tax regime is beneficial.

In case an individual claims lower deductions for tax savings, towards health insurance, investment in NPS and so on, the new regime will be more beneficial as against individuals who utilise the tax saving investments.

Also individuals with an income bracket between Rs.5-10 Lakh with lower claim of deductions will benefit from the new regime whereas individuals falling under higher income tax bracket above Rs.15 lakh of income per annum can benefit more from the existing regime by making tax saving investments.

It is important to note that each taxpayer should calculate income tax, taking into account their tax-saving investments and then choose the regime.

House property loss under the new tax regime

House property loss under the new tax regime

In case of a self-occupied property, you cannot claim a deduction on interest for a housing loan under the new tax regime. The deduction of Rs 2.00 lakh allowed in the existing system is not available in the new tax regime. Also, you cannot set-off the loss of Rs 2 lakh from house property from your salary income.

If you have let-out a house property, you can claim a deduction for interest paid on the housing loan. Do note that the new tax regime restricts the deduction to the taxable rent received from the property as against the old regime. In the new regime, you cannot set-off the loss arising from the house property due to excess of interest paid over the rental income. Also, you cannot carry forward the loss from house property to future years for set off.

Deductions for business expenditure not allowed under the new regime

Deductions for business expenditure not allowed under the new regime

Deductions and exemptions not allowed for business income:

- Additional depreciation under section 32.

- Investment allowance under section 32AD

- Sector-specific business deductions under section 33AB and 33ABA

- Expenditure on scientific research under section 35

- Capital expenditure under section 35AD

- Exemption under section 10AA for SEZ units

Unabsorbed depreciation and business loss under the new regime

Unabsorbed depreciation and business loss under the new regime

In the case of a business income, an individual or HUF cannot claim set-off of the brought forward business loss or unabsorbed depreciation.

The deductions not available under the new regime to the extent they relate to deductions/exemptions withdrawn.

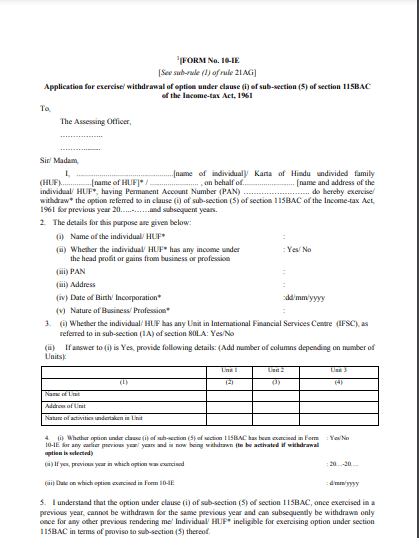

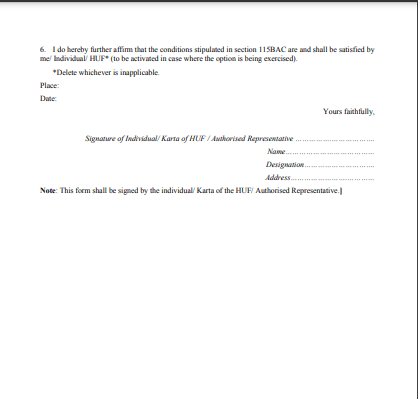

Form 10IE- Option to choose New Tax Regime

Form 10IE- Option to choose New Tax Regime

The finance ministry introduced a ‘New tax regime’ in the Finance Act 2020. Form 10IE is a declaration made by the return filers for choosing the ‘New tax regime’ So first, let us understand what do you mean by the new tax regime?

A tax regime refers to the computation of the individual’s income tax liability after considering all the deductions and tax benefits.

What is the old tax regime or existing tax regime?

What is the old tax regime or existing tax regime?

When we refer to the old/existing tax regime it means the tax on the income which is calculated as per the old tax slabs.

Under this regime, various levels of income are taxed according to slab available after considering all the deductions under Chapter VIA (such as deduction under section 80C, 80D, etc) as well as other tax benefits such as HRA, LTA and many others as allowed in the Income Tax Act 1961.

The existing regime levies tax at 3 levels i.e 5% tax on income between Rs 2.5 Lakh-Rs.5.00 Lakh, 20% tax on income between Rs.5.00 Lakh to Rs. 10 Lakh and 30% tax on income above Rs. 10 Lakhs. A 4% education cess is levied on the tax calculated on the above.

Applicability of New tax regime

Applicability of New tax regime

The new tax regime is applicable from the FY 2020-21, i.e. AY 2021-22. The choice between ‘New tax regime’ and ‘Old tax regime’ is available to individuals and HUF, which can be opted by filing Form 10IE.

How to provide the declaration of choice between both regimes?

How to provide the declaration of choice between both regimes?

If you are salaried, your employer might ask for a declaration from you to choose between the old or new tax regime.

How to inform the IT department of the selection of the tax regime?

How to inform the IT department of the selection of the tax regime?

Time limit for filing form 10IE

Time limit for filing form 10IE

For individuals with business income, Form 10IE can be filed before the due date of filing of ITR, i.e. 31st July or another date (in case due date is extended by the government)

For individuals having a salary income, Form 10IE can be submitted before or at the time of filing of ITR.

Contents of Form 10IE

Contents of Form 10IE

Basic details required to file Form 10IE are mentioned below:

- Name of the individual / HUF

- Confirmation of whether the individual or HUF have any income under ‘Profit or gains from business and profession.

- PAN number

- Address

- Date of birth/ date of incorporation

- Nature of business/ profession (Mandatory in case of business income)

- Confirmation in ‘yes/no’ of whether the taxpayer has any unit in IFSC (International financial service centre) as mentioned in sub-section (1A) of section 80LA. Suppose the answer is yes, then details of the unit to be provided.

- Details of any previous Form 10IE filed.

- Declaration

How to switch between Old and New tax regime?

How to switch between Old and New tax regime?

E-filing of Form 10IE

E-filing of Form 10IE

Form 10IE is required to be filed in an electronic form.

Taxpayers can file the form through the income tax department portal to opt for the new tax regime for FY 2020-21 and onwards.

The form will be filed using either the digital signature or through an electronic verification code (i.e EVC). The income tax department is yet to notify the procedure of filling and verifying the form.

Frequently Asked Questions

What if I forget to file Form 10IE?

If the taxpayers forget to fill the Form 10IE before or at the time of filing of ITR, the taxpayer will be disallowed to use the benefit of the concessional tax rates of the new tax regime. The income tax department will calculate tax based on the old/ existing tax regime.

Can I choose to file my return with a new tax regime if I have opted for the old tax regime for TDS deduction by my employer?

Only salaried individuals can opt out of any of the regimes every year. Also, the taxpayer is free to choose a different regime than he/she chose for TDS deduction with the employer, i.e. the employee can file an ITR using a different regime than the one he opted for before.

Which is better between the old tax regime and the new tax regime?

No single regime is beneficial for all. Both the regimes come with their benefits and shortcomings. However, we can give you some insight into both the regimes :

- The new tax regime is expected to largely benefit taxpayers who have a taxable income up to Rs 15 lakh whereas in the case of high-income earners above Rs. 15 lakhs, the old regime would be a better option.

- Also, as the new income tax regime does not allow any tax benefits or deductions, it is beneficial for people who make low investments. As the new regime offers seven lower income tax slabs, anyone paying taxes without claiming tax deductions can benefit from paying a lower rate of tax under the new tax regime.

- That being said, if you already have in place a financial plan by making investments in tax-saving instruments; medical and life insurance; making payments of children’s tuition fees; payment of EMIs on education loan; buying a house with a home loan; and so on, the old regime helps you with higher tax deductions and lower tax outgo.

Hence, it is advisable to do a comparative evaluation and analysis under both regimes and then choose the most beneficial one as it may vary from person to person.